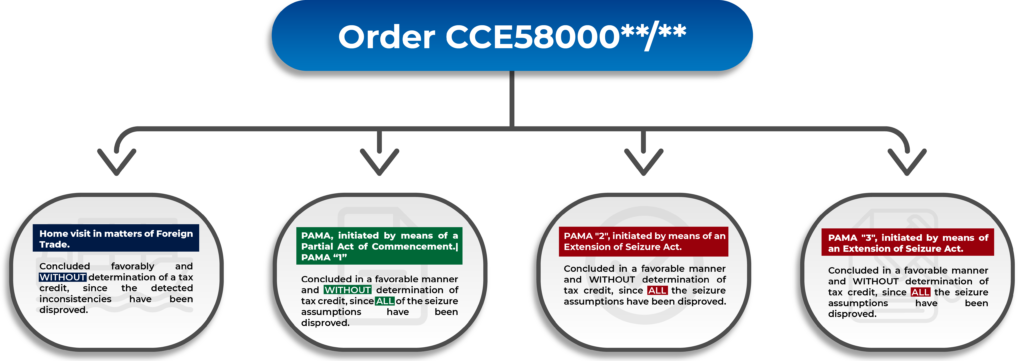

By means of the order for a field visit contained in the official letter 110-08-01-00-00-**, with order number CCE58000**/** , issued within the file 7S.-2 ****, issued by the North Pacific Decentralized Administration of Foreign Trade Audit, under the General Administration of Foreign Trade Audit, of the Tax Administration Service (hereinafter the authority), the company was ordered to carry out the audit procedure provided for in numeral 42 section III of the Federal Fiscal Code – DOMICILIARY VISIT-; with the purpose of verifying compliance with the tax and customs provisions to which it is subject as a direct subject in matters of Exports, Customs Processing Fees, Value Added Tax, as well as to verify the legal importation, possession or stay in the country of the merchandise of foreign origin and compliance with non-tariff regulations or restrictions and official Mexican standards.

, issued within the file 7S.-2 ****, issued by the North Pacific Decentralized Administration of Foreign Trade Audit, under the General Administration of Foreign Trade Audit, of the Tax Administration Service (hereinafter the authority), the company was ordered to carry out the audit procedure provided for in numeral 42 section III of the Federal Fiscal Code – DOMICILIARY VISIT-; with the purpose of verifying compliance with the tax and customs provisions to which it is subject as a direct subject in matters of Exports, Customs Processing Fees, Value Added Tax, as well as to verify the legal importation, possession or stay in the country of the merchandise of foreign origin and compliance with non-tariff regulations or restrictions and official Mexican standards.

a) PRECAUTIONARY SEIZURE – PAMA

As a result of the above, through the Partial Act of Initiation, the Field Visit Procedure ordered in the official notice described in the previous point was notified and initiated.

60 ASSETS SEIZED IN PRECAUTIONARY MEASURES.

60 ASSETS SEIZED IN PRECAUTIONARY MEASURES.

Since at the beginning of the procedure, foreign merchandise was detected at the company’s tax domicile, and since at that time the corresponding documents were not presented to prove its legal stay, possession and/or importation, the precautionary seizure of the foreign fixed assets inventoried in cases 01 to 60 was determined. With this, the Administrative Procedure in Customs Matters (PAMA) was opened independently, as foreseen in numeral 155 of the Customs Law.

Subsequently, as a result of the field visit order applied to the company, an additional act of extension was issued, notifying the seizure of the goods located at two (2) of the company’s domiciles:

33 ASSETS SEIZED IN PRECAUTIONARY MEASURES.

25 ASSETS SEIZED IN PRECAUTIONARY MEASURES.

It should be noted that in the case of the Foreign Trade Field Visit Procedure, two autonomous procedures are opened, one of which is referred to in number 155 of the Customs Law, and refers to the Administrative Procedure in Customs Matters, in which the seizure of assets was carried out, and the other is the Foreign Trade Field Visit or audit procedure.

one of which is referred to in number 155 of the Customs Law, and refers to the Administrative Procedure in Customs Matters, in which the seizure of assets was carried out, and the other is the Foreign Trade Field Visit or audit procedure.

b) FIELD VISIT IN FOREIGN TRADE MATTERS

As part of the conclusion stages of the home visit procedure, by means of the LAST PARTIAL REPORT of the procedure, the irregularities allegedly detected at the company’s expense and their possible legal consequences were disclosed:

In summary, the inconsistencies detected by the audit authority are as follows:

Chapter I.

A) Inaccurate data (Value Added)

For the period reviewed, it was observed that in 3,892 cases of goods manufactured, transformed and/or repaired for export, there were 30 inconsistent customs declarations, in which the amount in the field “VAL. AGREG.” the amount was declared as “0”.

Chapter II.

A) Omission in the return of temporarily imported goods

For the period under review, it is presumed that the irregularity of omission in the return abroad of the various goods imported temporarily, thereby omitting the General Import Tax, has been configured. 6273 cases.

B) Inaccurate data (Value Added)

For the period reviewed, in which it was observed that in 1587 cases of goods manufactured, transformed and/or repaired for export there were inconsistencies in 27 customs declarations, in which it was declared in the field “VAL. AGREG.” the amount in quantity “0”.

C) Inaccurate general data (Identifiers)

For the period reviewed, it was observed that in 21 export cases the identifier ¨DE” (WASTE) was not declared completely and correctly.

It should be noted that these inconsistencies resulted in a presumption against the company, calculated by the authority for omission of taxes and fines in the amount of $2’115,****,***.00 pesos (figures in billions, expressed with *** due to confidentiality of the information), which if not solved, would be determined an updated tax credit in that amount.

A) PRECAUTIONARY SEIZURE – PAMA

By virtue of the foregoing, immediately after the date on which we were entrusted with the attention of the matter, the following actions were carried out in order to disprove the assumptions for which the precautionary seizure of the fixed assets/machinery had been determined.

By virtue of the foregoing, immediately after the date on which we were entrusted with the attention of the matter, the following actions were carried out in order to disprove the assumptions for which the precautionary seizure of the fixed assets/machinery had been determined.

a) Within the established legal term, in accordance with the provisions of numbers 1, 43, 46, 150 and 155 of the Customs Law in direct relation with 1, 8, 14 and 16 of the Political Constitution of Mexico, the allegations and evidence required by law in each of the proceedings were offered and exhibited, which were sufficient to disprove the grounds that allegedly gave rise to the decree of the precautionary seizure. Based on this, the following were made:

-

- Comprehensive analysis of the information and/or customs documentation used to prove the legal stay and/or possession of the goods, for each of the cases seized in a precautionary manner in each PAMA.

- Implementation of an initial diagnostic audit to determine the viability of the information available to the company.

- Daily development of work meetings with the company to formulate and determine the strategy to be followed.

- Advice on the integration of documents and information to be submitted to the authority and formulation of legal strategy positions with respect to those documents that were considered insufficient to disprove the grounds for seizure.

- Preparation of the legal defense briefs, with which all the relevant evidence was presented in order to disprove the seizure assumptions, making a thorough confirmation that each document corresponded to each case.

- Presentation of the documents before the authority.

- Follow-up meetings with the authority together with representatives of the company, in which the solution of the matter was managed.

- It should be noted that in order to prove the legal stay and/or possession of the seized cases, and since in some of the cases it was applicable, the company was also able to assert various benefits that the company has since it is certified under the AEO and VAT and IEPS modality.

The foregoing, given that the Company counts and has counted since August 2005 and within the period of importation of seized fixed assets with the Certification of Companies in the Authorized Economic Operator (AEO) modality, importer and/or exporter item as well as with the VAT and IEPS Certification; For those cases in which the supporting documentation was not sufficient to refute the assumptions of embargo (22 of 118 cases), it was established that the embargoed goods were correctly imported, complying with all the formalities of the procedure; evidencing then that the documents exhibited to prove the legal stay and/or possession (invoice and petition) were sufficient to distort the assumptions of precautionary seizure, since said documents were processed under the protection of the benefits granted by the aforementioned certifications, which always they were and have been in force in favor of the company; since the company, through its foreign trade area, carries out active and permanent work to maintain the continuity of the aforementioned certifications.

Since the Company has had since August 2005 and within the period of the importation of the seized fixed assets with the Certification of Companies in the Authorized Economic Operator (AEO) modality, importer and/or exporter category, as well as with the VAT and IEPS Certification; it was established for those cases in which the supporting documentation was not sufficient to disprove the seizure assumptions (22 of 118 cases), that the seized goods were correctly imported complying with all the formalities of the procedure; It was then evidenced that the documents exhibited to prove the legal stay and/or possession (invoice and customs declaration) were sufficient to disprove the assumptions of the precautionary seizure, since said documents were processed under the protection of the benefits granted by the aforementioned certifications, which were always and have always been in force in favor of the company, since the company, through its foreign trade area, carries out an active and permanent work to maintain the continuity of said certifications.

In fact, one of the main benefits granted by these certifications and which was effectively asserted, is the ease of customs clearance of the goods for their temporary import or introduction, according to the system they operate under, without declaring or transmitting in the customs declaration, electronic document, invoice, shipping document or attached list, the serial, model, part or brand numbers; Therefore, it was demonstrated that the documents exhibited fully disproved the assumptions of the seizure and also, that the company fully complied with the obligations regarding inventory control ANNEX 24, as demonstrated before the authority.

With regard to the other seized cases, the corresponding documentary supports were integrated, mainly the import customs declaration and commercial invoice, with which the seizure assumptions were reliably disproved, in terms of number 146 of the Customs Law.

b) FIELD VISIT – FOREIGN TRADE

2. Immediately, the legal defense strategy was prepared to disprove the irregularities detected.

a) An intensive internal audit procedure was implemented in order to integrate the documentary support to disprove the irregularities detected.

b) Regarding the inconsistencies in ANNEX 24, the Stratego team began a very thorough procedure of automatic and manual review of the 6,273 cases of Annex 24 that were identified with inconsistencies, proceeding to correct them and corroborating the elements to resolve the irregularities detected. It is worth mentioning that the correction of this total of cases represented 536 hours of continuous work among different members of our Audit area.

c) Regarding the other inconsistencies detected (Inaccurate general data (Identifiers) and Inaccurate data (Aggregate Value), one by one the documentary supports were collected that reliably disproved the presumptions made by the authority and the legal arguments were formulated to support the refutation of such inconsistencies.

d) Subsequently, the legal defense briefs were prepared and presented, with which the detected irregularities were proven to have been disproved.

e) Following the above, personal representations were made to the authority to follow up on the promotions, supports and allegations presented.

a) PRECAUTIONARY SEIZURE- PAMA

As a result of our intervention and the legal strategies implemented; regarding the three (3) Administrative Proceedings of Precautionary Seizure (PAMA) by means of different official letters number 110-08-01-00-*** , issued by the Audit Administration, it was definitively resolved in favor of the company that the assumptions of precautionary seizure were disproved, for ALL the seized cases; consequently, the seizures made were left without effect and no sanctions were imposed and no tax credits were determined to be charged to the company.

In this regard, these proceedings were resolved FAVORABLY at the administrative stage.

c) FIELD VISIT

As a result of the strategies implemented, by means of a FINAL REPORT, the auditing authority determined in the first instance that the irregularities detected in  ANNEX 24 (assumptions of no return) had been SOLVED in their entirety, thus obtaining a very significant favorable result, since said irregularities made up the highest percentage of the cases detected.

ANNEX 24 (assumptions of no return) had been SOLVED in their entirety, thus obtaining a very significant favorable result, since said irregularities made up the highest percentage of the cases detected.

By means of resolution contained in official letter number 110-08-****, the authority resolved to consider that ALL the irregularities detected against the company had been disproved and, therefore, the predetermined tax credit was null and void.

In this regard, these proceedings were resolved FAVORABLY at the administrative stage.

I. Regarding the 3 (three) Administrative Proceedings of precautionary seizure:

I. Regarding the 3 (three) Administrative Proceedings of precautionary seizure:

A favorable resolution was obtained at the administrative stage for each proceeding, avoiding the payment of the tax credits predetermined by the authority and ensuring the company’s ownership of the

The payment of the tax credits predetermined by the authority was avoided, and the ownership of the seized merchandise was secured in favor of the company, as well as the continuity of its IMMEX Program.

II. Regarding the Field Visit procedure:

A favorable resolution was obtained in the administrative stage, avoiding the determination and possible payment of a predetermined tax credit in the amount of $2′ 115, ***, ***.** (figures in billions, expressed with – due to confidentiality of the information).

With the above, we also indirectly ENSURED THE CONTINUITY of our client’s DIFFERENT PROGRAMS AND AUTHORIZATIONS:

- IMMEX

- OEA

- VAT and IEPS certification

- Importers register

- Register of Exporters

- Digital seals

- Among others

Those which, upon definitive determination of the tax credit, would have been suspended or cancelled as a direct consequence of the debt owed by the company.

However, with the actions taken by our Firm, the aforementioned audit procedure was resolved in the ADMINISTRATIVE stage WITHOUT the determination of tax credits or the imposition of penalties.

Stratego’s established proficiency in fiscal and international trade areas positions us as your go-to resource. Should you require clarification or assistance regarding your operations, do not hesitate to get in touch.

Undoubtedly, obtaining all these favorable resolutions at the administrative stage is an unprecedented success story. In addition to ensuring the security and continuity of the company, by resolving these procedures in the administrative stage, it avoided the the opening of new procedures such as lawsuits or controversies that would have had to be filed against the tax credits that would have been determined.